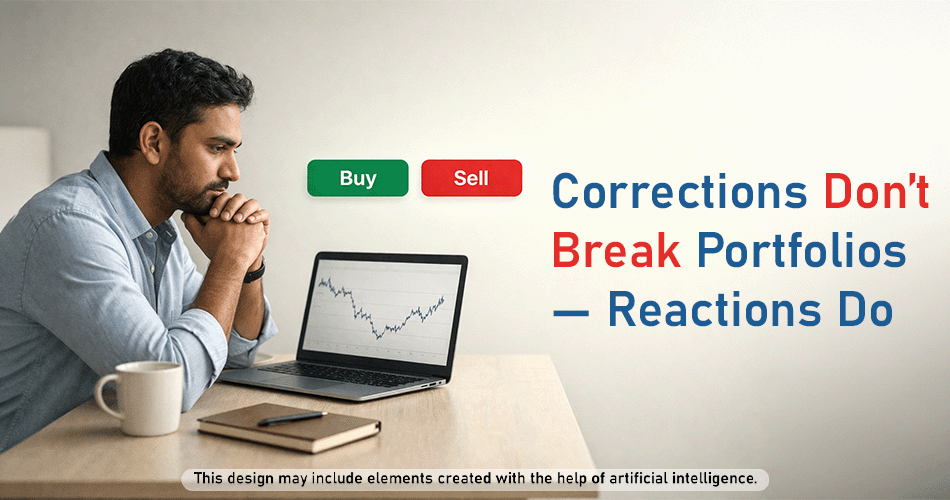

6 Habits That Quietly Destroy Investment Returns

In every conversation about mutual funds, risk comes up early. What is the risk in this fund? How much can the market fall? What if there is a global crisis? These are important questions, and they deserve serious answers. But there is a risk that almost never gets discussed- not in client meetings, not in fund factsheets, not in annual reviews. It is the risk of the investor’ own behaviour. The impulse to compare. The urge to switch. The instinct to stop investing when staying invested matters the most. This risk does not appear in any scheme document. Yet it quietly erodes more wealth than any market correction ever has. Ask any experienced MF distributor what holds investors back, and the answer is rarely the market. It is almost always something the investor did- or stopped doing- at the wrong time. Here are six such habits. 1. Measuring Your Returns Against Someone Else’ A colleague mentions a 40% return from a small-cap fund. A relative forwards a screenshot of their portfolio gains. Suddenly, a well-constructed, diversified portfolio delivering 12-13% feels inadequate. What investors hear at dinner tables and in WhatsApp groups is never the full picture. The losses are never forwarded. The concentration risk is never mentioned. The sleepless nights are never part of the story. Comparing returns without comparing the risk taken, the time horizon, or the purpose behind the investment is like comparing a Test match innings with a T20 cameo. The formats are entirely different, and so are the stakes. The only return that should matter is whether the portfolio is on track for its intended purpose- not whether it beat someone else’. 2. Chasing Last Year’ Top-Ranked Fund This comes up in almost every portfolio review conversation: “This fund was ranked number one last year- why am I not in it?” What follows is predictable. Exit the current scheme. Enter last year’ topper. Hope the performance repeats. It rarely does. Fund rankings are rearview mirrors, not windshields. The market cycle, sector rotation, and investment style that produced one year’ outperformance almost never repeat in the same sequence. Data consistently shows that the rank-1 fund in any given year rarely holds that position in the second or third year. And every switch comes at a real cost- exit loads, capital gains tax, and most importantly, a reset of the compounding clock. Over a decade, four or five such switches can quietly erode 1.5-2% of the total corpus. That is not a strategy. That is an expensive reaction to a backward-looking number. 3. Stopping the SIP When Markets Fall This is perhaps the most self-defeating habit in investing. And the most common. A SIP is designed to work because markets fluctuate- falling NAVs mean more units purchased at lower prices, which is precisely what builds wealth over time. Stopping a SIP during a correction is like closing the shop on the day customers finally walk in. Industry data shows that a significant proportion of SIPs are discontinued within the first three years, often during market downturns- the exact window when continuing would have delivered the greatest long-term benefit. The investors who stayed the course through 2008, 2020, and 2022 did not do so because the market felt safe. They understood something most others missed: discomfort is the price of compounding. 4. Investing Without Knowing Why A surprising number of investors start a SIP because someone suggested it, or because an app made it easy. The amount is round- ₹5,000. The fund is whatever showed up first. The reason? Vague. Without a defined purpose- a child’ higher education, a home, retirement- there is no framework for choosing the right fund category, the right time horizon, or the right amount. And when markets correct, there is no anchor to hold onto. An investor saving for a child’ college in 2035 can absorb a 15% correction in 2026 without flinching, because the destination is clear and the runway is long enough. Without that clarity, every dip feels like a crisis. Every headline becomes a reason to exit. 5. Checking the Portfolio Every Day Technology has made portfolio tracking effortless. But effortless access and useful access are not the same thing. An investor who checks the portfolio daily is not staying informed- they are exposing themselves to noise. A 1% dip on a Tuesday. A 0.5% recovery on Wednesday. None of it has any bearing on where the portfolio will be in five or ten years. Yet each data point triggers an emotional response, and enough emotional responses eventually trigger a bad decision. Research in behavioural finance has shown this repeatedly- the more frequently investors observe their portfolio, the more likely they are to make impulsive changes. The best portfolios are often the ones reviewed once a year- not once an hour. Watching the scoreboard after every ball does not help win a Test match. 6. Waiting for the ‘Right Time’ to Start Markets are at a high- wait for a correction. Markets are falling- wait for stability. The economy is uncertain- wait for clarity. There is always a reason to wait. The “right time” never quite arrives. Historical data across 25 years of the BSE Sensex shows that investors who began investing at market peaks and stayed invested for seven years or more earned positive returns in virtually every instance. The cost of waiting has almost always exceeded the cost of entering at what felt like the wrong time. (Source: BSE | Daily Rolling Returns: Jan 2001 – Dec 2025) The Quiet Truth None of these habits feel dangerous in the moment. Comparing returns feels natural. Switching to a top-ranked fund feels smart. Stopping a SIP during a fall feels prudent. But compounded over 10 or 15 years, these six habits quietly transfer wealth from the impatient to the disciplined. The investors who build the largest corpuses are not necessarily the ones who found the best fund. They are the ones who stayed with a sensible portfolio, kept their SIPs